“The hardest thing in the world to understand is the income tax,” said the great Albert Einstein. If he could not understand the tax labyrinth, who could possibly master it? On that note we explore below what goes on in the Indian start-up scenario when it comes to paying taxes.

As an employee your taxes are straight forward, you receive your paycheck after paying taxes. However, as an entrepreneur you receive full payment and then pay the taxes. And as an entrepreneur you have the advantage of making use of the several tax benefits schemes that reduce your tax outflow. To begin with, here is a roster of prominent tax saving features for entrepreneurs which you can use for an intelligent conversation with your auditor.

‘‘

As an entrepreneur you have the advantage of making use of the several tax benefits schemes that reduce your tax outflow.

Prominent tax saving features for entrepreneurs

Family First

Hiring family members in key positions is an advantageous proposition. And if these members do not have other sources of income, then they can be paid Rs 2,50,000 a year and they are not liable to pay tax. These salaries can be accounted as a cost to the company, thereby the taxable income is reduced and as a result the tax pay out as well.

More Marketing

It is given knowledge that marketing efforts propel the business forward and afford you expansion opportunities. Also, digital marketing has gained traction and businesses can leverage this to increase overall profitability and mark these marketing expenses as cost to the company, as these expenses qualify for tax deductions.

Travel Time

If you are travelling on business, then it would be worthwhile to expense it to your company account. This is considered a business expense and can be deducted from the taxable income of the company.

Utilize Utilities

Tax burden can be brought down significantly by some of the basic utilities that every business spends money on – Preliminary expenses which are incurred during the setup of the entity. Convenience expenses which are incurred because of phone bills, vehicles and salaries. If you are in a home office set up, then electricity and internet charges are also deductible from tax.

Health Hazards

The medical insurance premiums of up to Rs 25,000 is claimable for tax deductions under Section 80D of the Income Tax Act, 1961. It includes your spouse, children, and parents under this. The caveat here is that this is not applicable if you are a start-up owner in parallel to being a full-time employee where the employer provides medical insurance coverage.

Give Good

Tax exemptions are applicable to when you make donations to the registered charities and funds such as the PM’s relief fund. In fact, you can also donate to a recognised political party to claim tax breaks.

Happy Homes

If you have a housing loan, you can claim tax deductions of up to Rs. 1,50,000 a year under Section 80C of the Income Tax Act. Kindly link your PAN with the company.

Downward Depreciation

Companies (under Section 35AD) installing new equipment and machinery that have been installed for over a year can claim up to 20% additional depreciation, in addition to the regular depreciation in the year they were put in use.

Cash Crazy

If you are still stuck with cash disbursements to employees, please stop. As this increases your taxability and you are bound to pay more taxes. Adhere to digital transactions and adopt healthy tax saving practices.

Tax Compliance

Under the Income Tax Act, the payers (entrepreneurs) are liable to deduct a TDS at the rate of 10% for availing any service from an individual or a corporate if the payment exceeds Rs. 30,000 annually. In case you fail to deduct the same the entire amount paid will not be considered as an expense to the entity.

Are you an Eligible Entrepreneur? Here is a Checklist for Self-Assessment

Take this reality check to see if you are an entrepreneur in the real sense of the term according to the Income Tax department.

- How old are you? You must be less than 10 years of age since formation.

- How rich are you? Your turnover has not crossed 100 crores in any previous years.

- What are your goals? You must be working to promote innovation, development of employment opportunities and wealth creation.

- How were you formed? You must not be in existence due to a breakup of a company already in existence.

- Which of the below best describes you?

Sole

Proprietorship

Partnership

LLPCompany

- What is your identity?

Do you have a PAN? This is your unique number allotted by the Income Tax Department.

Do you have a TAN? This is required for TDS related compliances.

Do you require a GST

Required if income exceeds 40 lakhs and above for businesses engaged in goods.

If income exceeds 20 lakhs and above for businesses engaged in services.

Do you have a professional tax registration?

Do you have a shop and establishment license?

Do you have industry specific regulatory approvals?

Do you have an Import Export Code (IEC)? Necessary if your entity is involved in the import or export of goods and services.

If you have ticked all the above and have the necessary paperwork in place for qualifying to be as an eligible start-up, then you are entitled to enjoy the following tax benefits:

Initial Stage Waiver

If your entity has been incorporated between 1 April 2016 to 1 April 2021, then you can avail deduction of 100% of profits for a block of 3 years in the first 7 years of incorporation.

Angel Tax Waiver

When a domestic company wants to issue shares to public at Fair Market Value (FMV), the valuation is determined by the merchant banker based on the future cash flows of the company. In case the company decides to issue shares at a higher price than the determined FMV, such excess is treated as angel tax. With the requisite declaration with DPIIT and subject to certain conditions, eligible start-ups are exempted from Angel tax.

Set Off Waiver

The Income Tax laws provide for carry forward and set off of business loss. Meaning the same can be reduced from the profits of the future years. An eligible start-up is not taxed for the losses incurred in the first 7 years, provided the shareholders holding shares in the year of loss continue to hold shares in the year of set off.

Capital Gains Waiver

Long term capital gains from transfer of residential properties are exempted from capital gains tax if the consideration that it is invested in the equity shares of the eligible start-up.

ESOP Waiver

Eligible start-ups issuing ESOPs to its employees on or after the 1 April 2020 enjoy tax relaxation on deduction of tax on such ESOPs.

‘‘

Tax burden can be brought down significantly by some of the basic utilities that every business spends money on.

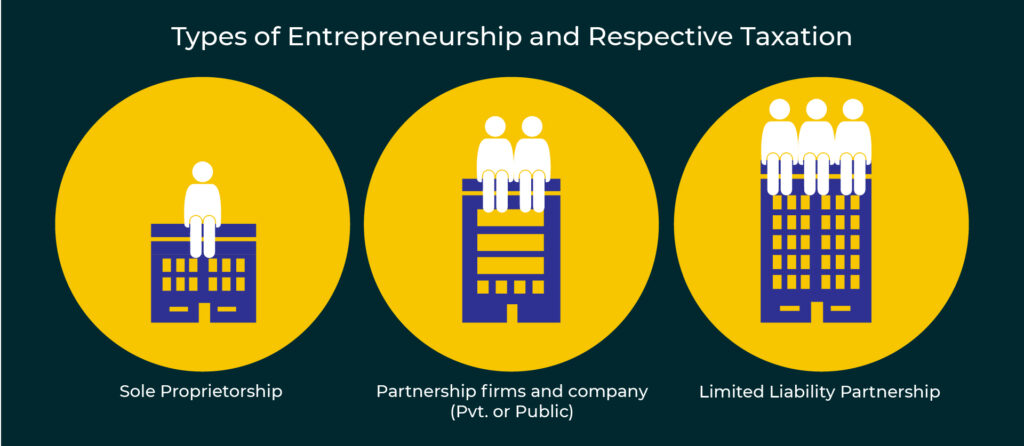

Types of Entrepreneurship and Respective Taxation

When it comes to entrepreneurship, which legal structure should your business take is a question you will have to think about. Not only is this important for your business to function, but it also has attendant tax benefits. In India, the three basic types of business structures that exist are:

Sole Proprietorship

Is a small and independent business owned by an individual, and they are unregistered and host hassle free operations. They are popular across the unorganized business sector and comprises merchants and traders with moderate incomes.

The taxation for sole proprietorship is conducted along with the business owner’s personal taxes. Therefore, the income generated from the business is added to the owner’s income after taking into consideration the deductions for tax, business expenses from the gross amount. They are entitled to enjoy the sole proprietorship tax deduction as per prevailing IT rules and upon the slab rates available to the taxable income.

Partnership firms and Company (Pvt. or Public)

Is a firm having more than one person conducting business under one entity and there are both registered and unregistered partnership firms. A registered partnership firm is one that is registered with the Registrar of Firms and has received a registration certificate for the same. And those that do not have a registration certificate from the Registrar of Firms is an unregistered partnership.

The taxation for partnership firm is required to pay the following tax percentages:

30% income tax – 12% surcharges where taxable income is above one crore rupees

Up to 12% on interest of capital is allowed

Health and Education Cess 4% of tax including surcharges

And unlike sole proprietorship the partnership firm has a different legal identity from that of its partners. Also, whether the partnership firm is registered or not they have to comply with tax norms. And they must also pay the alternate minimum tax which cannot be less than 18.5% of the adjusted total income.

Limited Liability Partnership (Hybrid of partnership and company)

With the rapid business growth across India, and the rise of the service sector there arose a need for a new form of organization that had the best of both Sole Proprietorship and Partnership. And this gave birth to the LLP which is a separate legal entity, and it stands separate from its founders. It has a minimum of two partners with no limit to the maximum number of partners. This type of hybrid organization is fairly easy to form and enjoys less restrictions and compliance as mandated by the Government.

The taxation for LLP is at a flat rate of 30% on its total income. There is a surcharge of 10% where total income exceeds one crore rupees. The amount of income-tax and the applicable surcharge shall be further increased by education cess and secondary and higher education cess calculated at the rate of 4% of such income-tax and surcharge.

Understand how to file your company’s ITR with these simple steps

Engage a practicing Chartered Accountant to audit your Financial Statements. This is mandated by the Income Tax Act Under Section 44AD.

Computation of Income Tax is the next crucial step. Calculate the difference between the total amount of Income Tax payable and amount paid as Advance tax or Tax deducted at source.

If the amount paid is greater than total income tax – get the refund.

If the amount paid is lesser than total income tax – pay the difference.

Obtain the Tax Audit report from the auditor who will provide the same in Form 3CA along with other details in Form 3CD.

File ITR once the auditor submits the audit report.

E-Filing: The entire filing process can be done only through the e-filing portal of the Income Tax website. The authentication of your signature is carried out through Aadhar Card and Bank Account numbers. Once your return is processed you will receive an e-assessment order from the IT department which will be notified to you via email. The refunds if any, are processed and dispatched within a reasonable timeframe. Your grievances can be registered through the same portal and you can also verify the tax deducted from various entities in Form No. 26AS, which is automatically populated in your IT return.