Don’t you just hate it when you go to a restaurant in anticipation of your favourite dish but they say, “Sorry, we ran out of stock.” A big disappointment for sure, but you might order the next best thing or go to another restaurant instead. This is exactly what happens if you do not have full control over your inventory or stock of finished products. You will lose customers to your competition and your profits will dip and you fail to supply what your customers want.

What Is Inventory Management?

A crucial part of the supply chain, inventory management is more complex than stocking your warehouse or feeding your procurement needs. Inventory refers to all physical items which flow in and out of a company. This includes the raw materials for production as well as the finished products for sales. Inventory management uses various methods and management techniques to handle the process of ordering, storing and using a company’s inventory.

Now, one may think that inventory management only concerns the raw materials that come into the flow of production, but it happens at all stages of a company’s line of production and supply chain. This includes raw materials, semi-finished goods, and even the finished products that are waiting somewhere in a company warehouse, waiting to be shipped off to the market.

Inventory management can be framed as having the right amount of goods or items necessary for a business to run successfully at any given time. On the one hand, there should be no shortages of inventory, but there the company should also avoid having so much in storage that it all goes to waste. Inventory management helps keep the balance.

‘‘

Without an inventory, a business will not have anything to offer its customers. Consider it the life blood of a business rather than just items.

How Does It Work And Why Is It Important?

Inventory management’s role in all this is to make sure that the company never runs out of these things. To make sure that does not happen, you need to track the market’s level of demand for your particular product or service. This gives you an idea of how often customers purchase your product/services and shows you how the pace at which inventory is should be ordered.

All this tracking and managing can be taken care of in two broad ways – manually or through software. With software the tracking is automated with minimal involvement of people. The manual method on the other hand, is almost entirely done by people.

Whatever path you choose for your company, it is apparent that inventory is key for any business to operate. Without it, even the supply chain, becomes just an empty system without anything to transfer, move or co-ordinate. Maintaining the right balance is crucial for any business, big or small. This is especially true for the likes of inventory-heavy industries such as the food business.

For instance, restaurants, need to make sure that they maintain a perfect balance at all times, while still maintaining quality (good food needs good ingredients). They have to have enough food that they do not run out on a busy night, but not so much that if business suddenly stops, (say, a sudden lockdown due to the pandemic) they are left sitting there with tons of food rotting in a storage unit.

Business foresight and ability to read the pulse on the market become vital. You do not want to suddenly find that there is a shortage – have the right amount of inventory, in the right place, at the right time. This is why inventory management is important, it lets you know when there is no more food in the kitchen.

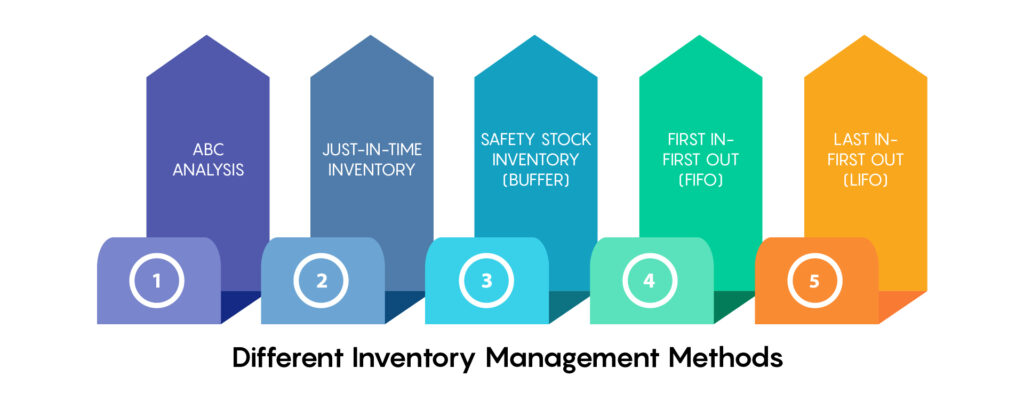

Which Inventory Method Works For You (Types Of Inventory)

ABC analysis

A technique that helps a company classify and manage its inventory based on the demand of the stock and the cost of holding or transporting it. The analysis tells us how fast the goods should be moved and how fast it needs to be reordered based on the demand. There are three different categories for this technique:

A level goods: The most popular and in-demand goods which will fly off the shelves and need to be restocked fast. These are not too expensive to store as these would be sold fast.

B level goods: Not so much in demand as the A-level goods but still enjoy a decent amount of demand. These are moderately expensive to store as they have to be stored for a longer period.

C level goods: Next come the laggards. C-level goods have the least demand, take up the maximum of storage space and, therefore, cost the most.

Just-in-time inventory

An extreme version of the EOQ system, it orders inventory when it is needed at the exact amount. It is a system that does not store much in reserve. Items are ordered only at the last minute.

Safety stock inventory (buffer)

Essentially keeping a backup stock for emergencies like a dip in the market, loss of revenue, loss of customers and so on. It will not work for perishable items like food though.

First in, first out (FIFO)

The oldest inventory in storage is sent out first for sales.

Last in, first out (LIFO)

The newest inventory is sent out first. Both help calculate the profitability of the inventory. You just have to pick one based on the demand in the market.

It is, indeed, a risky method but has a high-reward capacity if done right. The key here is to hire an inventory manager who understands the market and has a proven track record to get the job done.

A quick example of these fundamental techniques applied successfully is Walmart, a brand that most of us are familiar with. The retail giant has over $32 billion in inventory across 70 different countries. To move this massive amount, the company relies on two things. It uses automation software to move the inventory up and down the supply chain, and it does not store the stock for a long period. To put it simply, everything is sold and shipped quickly to make the flow faster and streamlined for maximum efficiency. The tracking software also helps reduce human error and keeps a tab on the numbers.

‘‘

The final aim of any inventory management system should be to get the products out to the customers as fast and as efficiently as possibile.

The Way Forward

Economic Order Quantity (EOQ)

This is the core of inventory management – order the minimum amount that you think your business needs to keep up with even the highest customer demands on any given day. The aim of this is to lower the cost of buying, storing and moving inventory as much as possible while staying competitive.

Minimum order quantity (MOQ)

On the other end of the spectrum, we have the minimum order technique. It is when a supplier is only willing to sell you a fixed minimum amount. This is the lowest quantity they can sell you while still making a profit if they sell lower than this, the supplier loses money. The purpose of this is so that suppliers can move inventory fast and skip over the businesses that want to bargain the price, which ultimately slows down the process.

The Materials Requirement Planning (MRP)

An inventory management method that is entirely dependent on the planning and forecasting abilities of inventory managers. They should be able to predict when a spike in demand is likely and place orders accordingly. If they overshoot or underestimate the prediction, it may result in severe losses for the company.

All of this can be achieved much more easily with the help of automation software. It is well worth the time and capital. It takes care of everything from tracking, budgeting, helps with planning for more inventory and also gives you an idea of how your sales are going to perform based on demand rates.

Trial runs help

Start with choosing the technique that best works for the specific type of industry that you want to be in and then, takes it for a spin. Conduct a practice run and ship some inventory around the system to make sure that everything works and flows nicely. Next, make use of reports, lots of reports. They help you keep a track of what went where and gives you a clear picture of how well your system performed in the past.

This is also why a trial run is needed moving forward as you do not want to do this when business is in full swing. You want to cover all your bases, that is to say, hire some extra staff. They do not have to be full-time; you can hire them part-time and keep them in reserve if demand ever goes through the roof and you suddenly need those extra hands. Speaking of covering all your bases, check out all your inventory – see how much you have to sell, how much you need to store, how much can be stored and for how long. That will give you a budget that you need to work within for the inventory system to work.