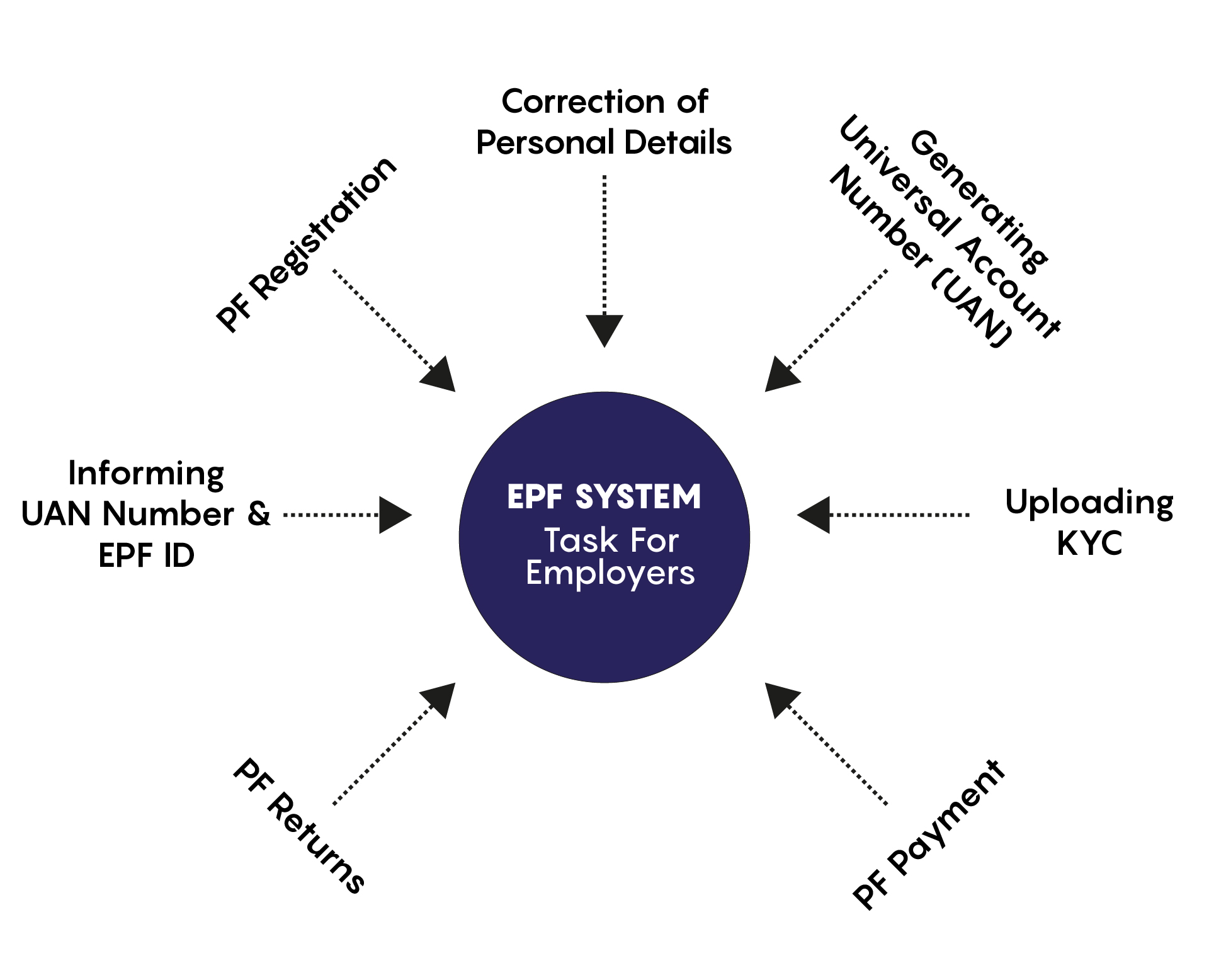

EPFO Tasks for Employers

We have established that any company with more than 20 employees has to register with the EPFO and contribute to the employees’ account. Now, you must know that as part of the process involved in EPF, the employer is supposed to do the following tasks while onboarding employees in her/his company:

PF Registration: The employer has to register the new employee into the EPF scheme with the help of Form 11. Form 11 is a self-declaration form that has to be filled and submitted by an employee at the time of joining a new organization. This form can be downloaded from the EPFO website, the link for the same is https://www.epfindia.gov.in/site_docs/PDFs/Downloads_PDFs/Form11Revised.pdf;

Correction of Personal Details: The employer has to verify the details filled by the employee. EPFO’s Universal Account Number (UAN) with the Aadhaar, the errors in the personal details of members like spelling errors have to be fixed by the employer;

Generating Universal Account Number (UAN): Now, the employer has to generate UAN for the new employee who does not have an existing UAN. To make a new UAN, the employer has to login UAN employer portal;

Uploading KYC: KYC is mandatory for the withdrawal of EPF. The EPFO needs the PAN, Bank account number and Aadhaar or other KYC details of each EPF member. Hence, it is the responsibility of the employer to record and upload the KYC details of her/his employees;

PF Payment: The employer has to pay the EPF contribution to the EPFO every month. The employer has to pay EPF contribution within 15 days of the next month. If the deadline is missed the company will be in the defaulter list and they have to pay a penalty for the default period;

PF Returns: An employee has to file a return of monthly payment by logging in to UAN employer portal and filling the Electronic Challan cum Return (ECR). The employer will give details of the employees, their salary as well as contribution. EPFO will then update the passbook of every employee. It is tallied with the aggregate of the EPF amount paid and an annual return is then filed by the employer;

Informing UAN number and EPF ID: The employer has to inform about the UAN and EPF member ID to its employee. It is usually printed in the salary slip. The employer persuades its employees to activate their UAN in order to do EPF related tasks online.